Retirement Life

20 March 2024

I need to save how much for retirement?!

As a country, we’re talking more and more about how much money we’ll need to have saved by the time we retire if we want the comfortable lifestyle many of us aspire to. It’s a valuable conversation, particularly in exposing younger generations to the importance of adopting a savings mentality, which will benefit them tremendously over the long term.

How much is enough?

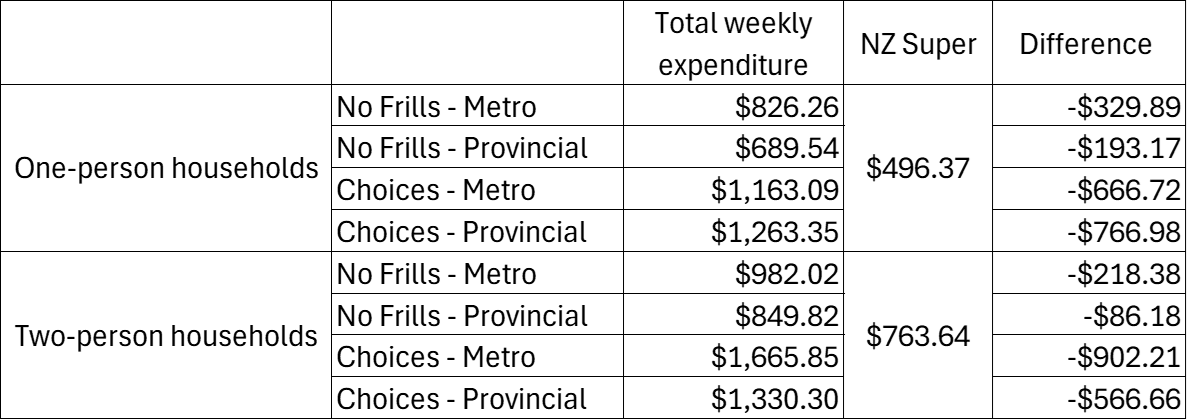

Every year, Massey University’s Financial Education Centre releases an updated set of Retirement Expenditure Guidelines (REGs), designed to give Kiwis saving for retirement an idea of how much money they might need to live a particular lifestyle post-work.

Given the soaring costs of living over the last year or two, you probably won’t be surprised to learn that retirement spending has increased by between 3.7% and 6.2% since last year, depending on whether you live in a one or two-person household and in a province or a city. It also confirms what most of us already know: NZ Superannuation is simply not enough.

REGs: Difference between spending and current rates of NZ Super

Calculate what you could draw in retirement.

Remember, they’re just a guide

While well-meaning and certainly valuable to those still earning, retirement spending data like this can be daunting if you’ve already retired or aren’t far away from it and are unlikely to be adding much more to your savings. That’s why it’s so important to remember that they’re just guidelines. They don’t reflect the enormous variation in individual circumstances and lifestyle goals.

In short, some people will find they get by spending less, while others will have plans that cost more. And most people won’t spend at the same rate throughout their retirement years, often spending more in the first ten years or so when they’re more active, with expenses falling in later years.

Behind the numbers

It’s also worth noting how the amounts are calculated. These REGs are based on the Household Expenditure Survey (HES) conducted every three years by Statistics NZ. The survey collates spending information from around 5,500 households around the country over a one-week period, so it might not always represent a typical week for all respondents.

The REGs use spending data from retirees only. On the years that Statistics NZ doesn’t conduct the survey, the REGs are simply adjusted to reflect inflation. Due to covid-related disruptions, the last HES was done in 2018/19 so the above retirement spending guidelines have only been inflation adjusted since then.

Create your own guidelines

When it comes to more tailored information that speaks directly to your circumstances, online calculators are a great resource. For instance, if you want to find out how much income you could expect based on your current or expected future savings, check out Lifetime Retirement Income’s income projection calculator. This lets you adjust for key variables like expected life span, tax, inflation and changing spending patterns over retirement.

For example, a woman with $100,000 in savings with a prescribed investor tax rate of 17.5% who plans to retire at 65 and expects to live into her 90s could expect to generate an extra $200 a fortnight on top of NZ Super.

It’s worth having a play with the calculator even if you still have years between you and retirement. The earlier you plan, the better prepared you’ll be to make the most of your post-work years.

Get in touch

If you have any questions about the income projection calculator, or the kind of products that are available to help manage your income needs in retirement, we’d love to hear from you. You can reach the Lifetime Retirement Income team at:

Take control of your retirement income

Written by:

Vanessa Glennie

Vanessa is Head of Communications at Lifetime Retirement Income. She’s an experienced investment writer, having spent more than a decade writing about financial markets in the global fund management industry.

Invest with Lifetime for a retirement income managed for living.